Скачать с ютуб Sharpe Ratio, Treynor Ratio and Jensen's Alpha (Calculations for CFA® and FRM® Exams) в хорошем качестве

Sharpe Ratio, Treynor Ratio and Jensen's Alpha (Calculations for CFA® and FRM® Exams)

3 года назад

Скачать бесплатно Sharpe Ratio, Treynor Ratio and Jensen's Alpha (Calculations for CFA® and FRM® Exams) в качестве 4к (2к / 1080p)

У нас вы можете посмотреть бесплатно Sharpe Ratio, Treynor Ratio and Jensen's Alpha (Calculations for CFA® and FRM® Exams) или скачать в максимальном доступном качестве, которое было загружено на ютуб. Для скачивания выберите вариант из формы ниже:

Загрузить музыку / рингтон Sharpe Ratio, Treynor Ratio and Jensen's Alpha (Calculations for CFA® and FRM® Exams) в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса savevideohd.ru

Sharpe Ratio, Treynor Ratio and Jensen's Alpha (Calculations for CFA® and FRM® Exams)

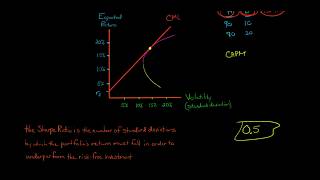

AnalystPrep's Concept Capsules for CFA® and FRM® Exams This series of video lessons is intended to review the main calculations required in your CFA and FRM exams. For Level I Video Lessons, Study Notes, Question Bank, CBT Mock Exams & More: https://analystprep.com/shop/cfa-leve... For FRM (Part I & Part II) Video Lessons, Study Notes, Question Bank, CBT Mock Exams & More: https://analystprep.com/shop/unlimite... AnalystPrep is an Official GARP-Approved Exam Preparation Provider Sharpe Ratio The Sharpe Ratio is defined as the portfolio risk premium divided by the portfolio risk. The Sharpe ratio, or reward-to-variability ratio, is the slope of the capital allocation line (CAL). The greater the slope (higher number) the better the asset. The Sharpe Ratio defines the risk in terms of standard deviation, which is a measure of total risk. Hence, it includes both systematic as well as unsystematic risk. Treynor Ratio The Treynor ratio is an extension of the Sharpe ratio that instead of using total risk uses beta or systematic risk in the denominator. As such, this is better suited to investors who hold diversified portfolios. As with the Sharpe ratio, the Treynor ratio requires positive numerators to give meaningful comparative results and, the Treynor ratio does not work for negative beta assets. Also, while both the Sharpe and Treynor ratios can rank portfolios, they do not provide information on whether the portfolios are better than the market portfolio or information about the degree of superiority of a higher ratio portfolio over a lower ratio portfolio. Jensen's Alpha Jensen's alpha is based on systematic risk. The daily returns of the portfolio are regressed against the daily returns of the market in order to compute a measure of this systematic risk in the same manner as the CAPM. The difference between the actual return of the portfolio and the calculated or modeled risk-adjusted return is a measure of performance relative to the market. If alpha is positive, the portfolio has outperformed the market whereas a negative value indicates underperformance. The values of alpha can also be used to rank portfolios or the managers of those portfolios with the alpha being a representation of the maximum an investor should pay for the active management of that portfolio.

Comments