Скачать с ютуб Accretion and dilution в хорошем качестве

Accretion and dilution

4 года назад

Скачать бесплатно Accretion and dilution в качестве 4к (2к / 1080p)

У нас вы можете посмотреть бесплатно Accretion and dilution или скачать в максимальном доступном качестве, которое было загружено на ютуб. Для скачивания выберите вариант из формы ниже:

Загрузить музыку / рингтон Accretion and dilution в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса savevideohd.ru

Accretion and dilution

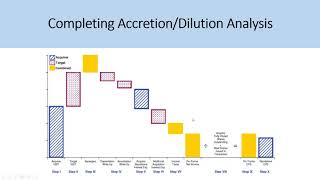

What is the meaning of accretion and dilution? Corporate executives often talk about accretion and dilution when explaining their capital allocation strategies to investors: “We identify and pursue accretive M&A opportunities”. Or when an actual merger or acquisition is announced: “the transaction is expected to be dilutive this year, and accretive thereafter”. What these executives refer to is the effect on a financial metric called Earnings Per Share, or EPS, which is simply the Net Income generated by a company divided by the number of its outstanding shares. • Earnings Per Share explained ⏱️TIMESTAMPS⏱️ 0:00 Accretion and dilution in mergers and acquisitions 0:38 EPS accretion example 1:15 EPS dilution example 1:52 Accretion dilution in acquisition decisions 3:02 Accretion dilution analysis 3:46 Drivers of accretion and dilution 4:59 Accretion dilution and non-GAAP EPS Here’s a numerical example of EPS accretion: the EPS forecast for the stand-alone company XYZ is $2.50 this year, $2.70 next year, and $3 two years from now. XYZ company is considering to buy ABC corporation. As a result of the transaction, the EPS is expected to go up by 2 cents this year, 3 cents next year, and 4 cents two years from now. This makes the expected EPS of the combined company after doing the deal higher than the expected EPS without doing the deal, which is called accretion. Here’s a numerical example of EPS dilution: the EPS forecast for the stand-alone company XYZ is the same $2.50 this year, $2.70 next year, and $3 two years from now. XYZ company is considering to buy DEF corporation. As a result of the transaction, the EPS is expected to be lowered by 4 cents this year, 3 cents next year, and 2 cents two years from now. This makes the expected EPS of the combined company after doing the deal lower than the expected EPS without doing the deal, which is called dilution. So which of the two companies should XYZ buy? Naïve EPS-focused executives and investors would say ABC, as the ABC deal is expected to be accretive to EPS. The better answer is: it depends! Let’s take a look at the business life cycle of acquisition targets ABC and DEF. Companies start off as embryonic or emerging, then go through growth, maturity, and ultimately aging and decline. Maybe ABC is a mature company that currently generates a good level of net income, but is getting close to its peak and has very few growth prospects. DEF on the other hand could be an embryonic company that has not generated any net income yet, but is about to launch a product that has the potential of generating billions of dollars in the future. Which of these companies would you like to buy? Once again, the answer is “it depends”, as for example we don’t know the acquisition price or the expected returns on the investment. But certainly we shouldn’t just look at accretion or dilution of EPS to decide! If the acquiring company issues new shares to finance the acquisition, increasing the share count by 5%, but in return is expected to be able to increase its net income by 10%, then the deal is labeled accretive as it increases #EPS. If the share count increases by 10%, and net income by just 5%, then the deal is labeled dilutive as it decreases EPS. Here’s a practical observation for you: in our debt-loaded economy, acquisitions are often financed with cash on hand and/or proceeds from debt financing. In that case, the number of shares in the denominator doesn’t change, and accretion – dilution analysis is really about trying to estimate the effect of the M&A transaction on net income. Here are some important factors to consider. Being able to add the existing or potential Net Income of the acquired company to your numbers, realizing cost synergies for example by integrating back-office functions, or realizing revenue synergies through more valuable complementary product portfolios, would all generate additional net income, and drive accretion. Having to absorb the expenses for amortization of Intangible Assets created in the deal, facing acquisition-related charges such as legal, regulatory, restructuring and integration costs, and paying interest on the incremental debt, would all decrease net income, and drive dilution. Each M&A deal has specific characteristics, sometimes the sum of these items is a net positive, sometimes a net negative. Philip de Vroe (The Finance Storyteller) aims to make accounting, finance and #investing enjoyable and easier to understand. Learn the business and accounting vocabulary to join the conversation with your CEO at your company. Understand how financial statements work in order to make better investing decisions. Philip delivers #financetraining in various formats: YouTube videos, classroom sessions, webinars, and business simulations. Connect with me through Linked In!

Comments