Скачать с ютуб GARCH model - volatility persistence in time series (Excel) в хорошем качестве

GARCH model - volatility persistence in time series (Excel)

3 года назад

Скачать бесплатно GARCH model - volatility persistence in time series (Excel) в качестве 4к (2к / 1080p)

У нас вы можете посмотреть бесплатно GARCH model - volatility persistence in time series (Excel) или скачать в максимальном доступном качестве, которое было загружено на ютуб. Для скачивания выберите вариант из формы ниже:

Загрузить музыку / рингтон GARCH model - volatility persistence in time series (Excel) в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса savevideohd.ru

GARCH model - volatility persistence in time series (Excel)

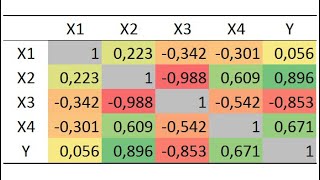

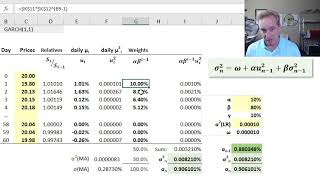

Generalised autoregressive conditional hereroskedasticity (GARCH) is an extension over ARCH that has been proposed by Tim Bollerslev in 1986. It allows for even more persistent volatility and is extremely useful, especially in high-frequency financial and economic time series. Today we will learn how to apply it in Excel and how to interpret its results. Econometrics is easy with NEDL! Please consider supporting NEDL on Patreon: / nedleducation

Comments