Скачать с ютуб DCC GARCH model: Multivariate variance persistence (Excel) в хорошем качестве

DCC GARCH model: Multivariate variance persistence (Excel)

3 года назад

Скачать бесплатно DCC GARCH model: Multivariate variance persistence (Excel) в качестве 4к (2к / 1080p)

У нас вы можете посмотреть бесплатно DCC GARCH model: Multivariate variance persistence (Excel) или скачать в максимальном доступном качестве, которое было загружено на ютуб. Для скачивания выберите вариант из формы ниже:

Загрузить музыку / рингтон DCC GARCH model: Multivariate variance persistence (Excel) в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса savevideohd.ru

DCC GARCH model: Multivariate variance persistence (Excel)

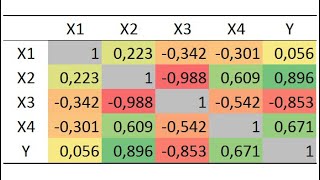

We all know returns and volatilities of assets are interconnected and correlated. And most of the time, this correlation is dynamic, posing significant challenges for portfolio and risk management. How to make sense of it? And is there a model that intertwines variance persistence and volatility clustering with the concept of time-varying correlation? Turns out there is! Today we are investigating the DCC (dynamic conditional correlation) GARCH - one of the most famous multivariate GARCH generalisations - and its application to modelling of interconnected volatility dynamics in time series. Don't forget to subscribe to NEDL and give this video a thumbs up for more videos in Finance! Please consider supporting NEDL on Patreon: / nedleducation

Comments